I’ve written a few posts on how the Philippines taxes income from capital gains and dividends from foreign stocks:

- How are foreign capital gains taxed in the Philippines?

- Are gains from US equity feeder funds taxable by the BIR?

It was confusing at first but I have since come to the conclusion that since there is no law or BIR ruling that specifically provides for fixed tax rates or exempts foreign capital gains and dividends, they fall into the catch-all category of “non-business/non-profession” income that will be taxed at ordinary graduated income rates. Still, I have few more questions.

Where do I enter foreign capital gains and dividends income on the income tax return form?

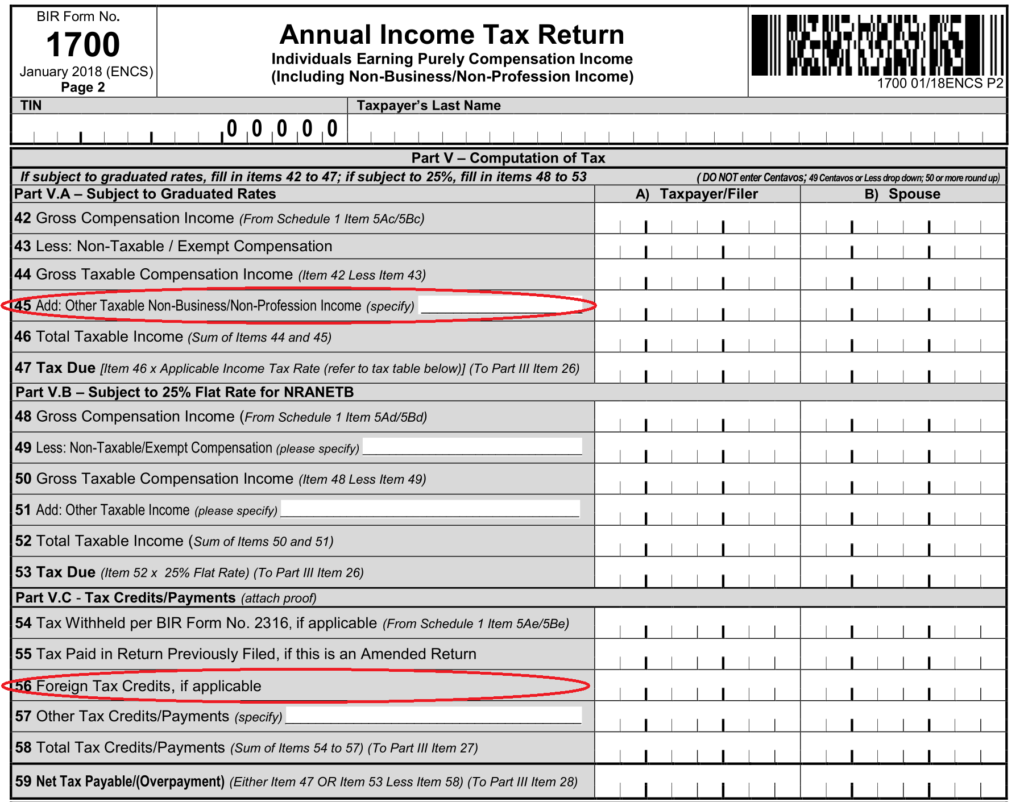

If I’m not mistaken, the only place you can enter this type of income is on Line 45 of Form 1700: Other Taxable Non-Business/Non-Profession Income. This appears to be the catch-all field for all other income that the BIR has not provided a final tax rate or exemption. What if you have different types of this income (e.g. foreign capital gains, foreign dividends, gambling income, foreign gifts)? Well, the BIR apparently did not imagine such possibility when they designed their forms. Strangely, there is no supporting documentation required for the amount you enter on Line 45.

Can foreign capital losses be used to offset foreign capital gains?

It seems obvious to think that if the government wants a share of your gains, it should also have a share in your losses. That’s how it works in the US, at least. Any capital loss can be used to reduce your net capital gains. If your losses exceed your gains, then you can deduct up to $3,000 of your net losses each year from the rest of your ordinary income. If your net losses exceed $3,000, then you can use the excess deduction in subsequent years.

Philippine tax authorities do not have any published rules on whether you can deduct losses from your gains, so legally this appears to be a gray area. Since no supporting documentation is required for the Line 45 amount, it’s probably safe to enter net gains.

Can net foreign capital loss be deducted from ordinary income?

Again, the BIR has no published rule that allows this kind of deduction. The likely answer is no.

Can foreign tax credits be used to offset Philippine tax liabilities?

Line 56 in Form 1700 allows one to enter foreign tax credits. I haven’t found any published BIR rule on how to properly claim foreign tax credits and if there are any limits to such claims. For example, the U.S. withholds 25% tax on dividends and 15% tax on interest. If your only income comes from dividends and falls within the <PHP 250,000 0% tax bracket, then I guess you cannot apply the foreign tax credit since no Philippine tax is due on the dividend income. But what if your total income now falls under the 20% bracket, can you claim the entire 25% foreign tax credit, or only up to 20%? Will it be different if you fall under higher tax brackets? I was not able to find the answer to these questions on the BIR website.

If any Philippine tax expert comes across this post, I’d like to hear your comments and corrections.

Leave a Reply