Home-country bias is the tendency of an investor to over-invest in his/her country’s domestic equity market in a scale that significantly exceeds the proportion of the size of the domestic market relative to the rest of the world.

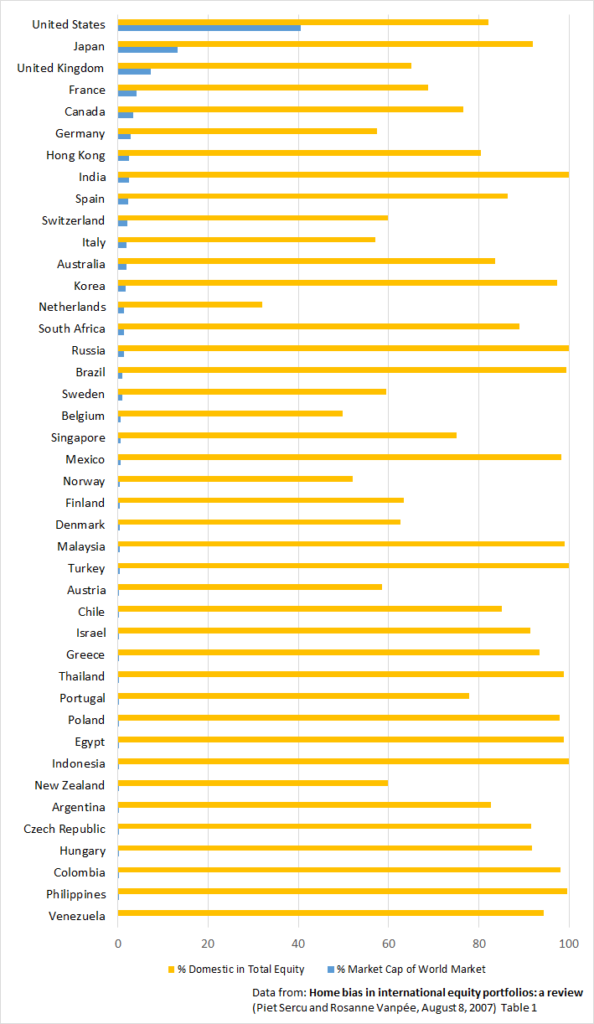

Considering that even Americans, whose own stock market is 40% to 50% of the world market, can be guilty of home-country bias, it is not a surprise that investors from much smaller markets like the Philippines also exhibit this behavior. This is shown in the chart below, which visualizes data collected by Sercu and Vanpée from CPIS (December 2005) and World Federation of Exchanges, in their paper, Home bias in international equity portfolios: a review. When that paper was published, Filipinos’ equity portfolios were 99.5% domestic while the domestic market was just 0.1% of the world market cap.

The Philippine market has grown since then, but home-country bias is still prevalent (Philippine HNWIs maintain strong home bias) even with the availability of UITF feeder funds that give access to some foreign ETFs. Since that article was published in 2017, a few more feeder funds have been launched by local funds.

There are local feeder funds that track U.S. indices like the S&P 500, but those expose you only to U.S. equities. But the easiest and simplest way to get exposure to international equities is through a single fund that tracks a benchmarks like the MSCI All Country World Index (ACWI) or FTSE Global All Cap Index. Both of these indices are market-capitalization weighted indices tracks all cap companies in both developed and emerging markets. Example funds include the iShares ACWI ETF which follows the ACWI index and the Vanguard VT (Total World) ETF that follows the FTSE Global All Cap Index. The table below shows typical country allocations for ACWI (as of November 20, 2019) and for VT (as of October 31, 2019).

| ACWI Country | % of acwi fund | vt country | % of vt fund |

|---|---|---|---|

| United States | 56.56 | United States | 55.00% |

| Japan | 7.3 | Japan | 7.80% |

| United Kingdom | 4.71 | United Kingdom | 5.00% |

| China | 3.68 | China | 3.50% |

| France | 3.36 | Canada | 3.00% |

| Canada | 2.98 | France | 3.00% |

| Switzerland | 2.71 | Switzerland | 2.60% |

| Germany | 2.57 | Germany | 2.50% |

| Australia | 2.01 | Australia | 2.20% |

| Taiwan | 1.43 | Taiwan | 1.60% |

| South Korea | 1.41 | South Korea | 1.40% |

| Netherlands | 1.16 | Netherlands | 1.10% |

| Hong Kong | 1.05 | Hong Kong | 1.10% |

| Other | 9.07 | Other | 10.20% |

Obviously, both market-capitalization weighted funds are dominated by US stocks, and around 10% come from emerging markets including China. Both funds also carry small holdings of blue-chip Philippine companies like SM, Ayala, and Jollibee, so buying such a fund will already get you exposure to the Philippine market. Philippine stocks account for 0.1% share in the VT fund. The biggest companies in both funds include the largest US tech companies like Microsoft, Apple, and Alphabet (Google).

Fortunately, there are now local feeder funds that have target funds that track the ACWI, FTSE Global All Cap indices, and other similar indices. Here are at least five of them:

| Fund Provider | Security Bank | BDO | BPI |

| Fund Name | SB Global Equity Index Feeder Fund | BDO Global Equity Index Feeder Fund | BPI Global Equity Fund-of-Funds |

| Benchmark | FTSE Global All Cap Index | MSCI World Index | MSCI World Index |

| Trust Fees | Class A 0.64% | 0.50% | 1.50% |

| Target Fund | Vanguard Total World Stock ETF | iShares World Equity Index Fund (LU) Class A2 USD | Wellington Global Quality Growth Fund (47.68%) SPDR S&P 500 ETF (20.57%) Wellington Strategic European Fund (11.34%) Wellington Global Health Care Fund (6.29%) |

| Target Fund Expense Ratio | 0.11% | 0.54% | ? |

| Minimum Investment | $1,000 | $500 | $500 |

| Additional Investment | $500 | $500 | $200 |

| Fund Provider | Metrobank | ATRAM |

| Fund Name | Metro World Equity Feeder Fund | ATRAM Global Equity Opportunity Feeder Fund |

| Benchmark | MSCI AC World NR | MSCI World Net Index |

| Trust Fees | 1% | 0.90% |

| Target Fund | Investec Global Strategic Equity Fund | Fidelity Funds – International Fund |

| Target Fund Expense Ratio | 1.58% | 1.05% |

| Minimum Investment | $2,000 | $1,000 |

| Additional Investment | $1,000 | $500 |

Only the SB Global Equity Index Feeder Fund tracks an ETF which tracks the FTSE Global All Cap Index. The rest appear to use mutual funds. ETFs are known for their low expense ratios. ETFs are also quite transparent with their holdings so for example, you can get a lot of information from the Vanguard VT ETF page.

The Metrobank feeder fund tracks a fund that uses the AC World Net Return index. I believe it’s the same as the ACWI index except that the AC World Net Return index assumes the dividends received are reinvested.

The BDO, BPI and ATRAM funds follow the MSCI World index which only covers developed markets, so they are not really fully global. The BPI feeder fund is a fund-of-funds so it has allocations of different funds within it. Its 5-year return appear to outperform its benchmark. The BPI fund’s trust fee is also expensive at 1.5%.

Since we want a fund that covers both developed developed and emerging markets, so we’re down to Security Bank and Metrobank’s feeder funds. Metrobank’s target fund also appear to have a high expense ratio. I’m biased towards ETFs so if I had to choose, I’ll probably go with Security Bank’s feeder fund that tracks the Vanguard VT ETF. I don’t know yet if I can totally get rid of home-country bias by not investing an extra portion directly into something like FMETF. What I know for sure is that allocation 100% of one’s portfolio only in equities in a small market like the Philippines is too limiting and also too risky.

(Needless to say, investing in foreign equities also exposes you to exchange rate risk. I’m also not yet completely sure if there are potential tax issues with these foreign feeder funds.)

Simple website, great content!